In March 2026, the Eurosystem reached a decisive milestone by launching the official Call for Expression of Interest for the digital euro pilot. Following the transition from theoretical investigation to technical readiness, the project is now moving toward concrete operational validation. As the 1st ranked framework contractor for the Secure Exchange of Payment Information (SEPI)[1] of the digital euro, which is required for the pilot phase starting in the second half of 2027, Senacor conducted a strategic analysis of the pilot requirements and the opportunities it presents for Payment Service Providers (PSPs). We aim to contribute to the industry dialogue on shaping the future of European payments and invite our clients and partners to engage with our views on this transformation. (Find us on LinkedIn)

The Foundation of Technical Readiness

This current momentum is the result of a disciplined multi-year journey that has seen the digital euro evolve from conceptual designs into a first viable draft. The foundation was laid by establishing the product architecture and functional requirements needed to ensure that the digital currency meets the needs of all European stakeholders. Over the past years, this theoretical work transitioned into intensive implementation planning, which included the drafting of a comprehensive rulebook to standardize operations and the selection of specialized technical infrastructure providers. One pillar of this development was the technical experimentation phase, where approximately 70 market participants, including Senacor, utilized a dedicated innovation platform to stress-test core features and various integration scenarios[2]. These continuous cycles of design and industry consultation have successfully moved the project from theoretical research to the very threshold of real-world validation.

From Concept to Reality: The Pilot Phase Begins

Following up on the previous innovation work, the Governing Council of the European Central Bank (ECB) made a landmark decision to officially progress the digital euro project into its next phase by introducing a comprehensive pilot program scheduled for a 12-month operational period beginning in the second half of 2027[3]. This pilot will utilize a „beta digital euro“- a version of the currency that replicates the final technical features and design specifications as accurately as possible. The goal is to validate functional designs, technical market readiness, and overall end-user experience through real transactions in a controlled environment. This upcoming pilot should not be seen as a mere test, but rather as a definitive opportunity for financial institutions to provide feedback and shape the future of European payments instead of merely adapting to them later.

The four relevant Use-Cases the Pilot revolves around

To turn this definitive opportunity into reality, the Eurosystem will perform a real stress-test of the „beta digital euro“ in a controlled yet realistic pilot environment. This phase moves beyond plain technical simulations to validate four primary use cases that represent the most essential payment activities for European citizens and businesses, which ensures that a harmonized user experience (UX) meets the high standards required for mass-market adoption. The pilot scenarios cover both Person-to-Person (P2P) and Person-to-Business (P2B) transactions across online, offline, and proximity contexts. While P2P includes remote transfers via unique identifiers (e.g., phone number or digital euro account number (DEAN) and offline near field communication (NFC) payments, where funds are exchanged directly between devices and settled instantly, P2B focuses on merchant payments at the physical point of sale (POS) via SoftPOS and in e-/m-commerce through integrated app and web flows, ensuring a seamless user experience.

How to be Part of the Digital Euro Pilot

The launch of the official Call for Expression of Interest in March 2026[4] marks the beginning of a highly competitive phase for financial institutions across the euro area.

With the application deadline set for 14th of May 2026, any institution that wants to apply must decide soon about the capacity in which they intend to operate within the pilot ecosystem and the type of role they want to take – a distributing role, an acquiring role, or even both. In a distributing role the institution focuses on individual end-users, taking responsibility for onboarding users to the „beta digital euro,“ managing their accounts, and enabling transactions through either a Eurosystem-provided app or a proprietary application integrated with the digital euro software development kit (SDK). Conversely, an acquiring role targets business end-users by providing merchants with acceptance solutions, such as SoftPOS for physical stores or dedicated interfaces for e-commerce platforms.

The selection process itself is structured into two tiers to ensure that only the most capable and representative institutions join the pilot. Basic eligibility requires that a provider hold a valid EU license to provide account-servicing payment services as a credit, payment, or electronic money institution. Furthermore, the applicant must demonstrate solid technical capabilities and the needed operational resilience. Once these basic requirements are confirmed, the Eurosystem evaluates candidates based on weighted criteria, including their market reach and geographic footprint to ensure a balanced representation across the euro area. Following the selection in June 2026, the chosen 25-30 participating PSPs will sign a Participation Agreement in July 2026 to formalize their commitment to shaping the next generation of European payments.

While the ECB encourages PSPs to apply for participation in the digital euro pilot, it acknowledges that PSPs may not be able to support all four use cases to the same degree. Therefore, in a March 2026 focus session, the ECB stated that applications that do not cover all use cases will nevertheless be accepted for consideration.[5]

What does this mean for the participating PSPs?

What does this mean for the participating PSPs?

Participating in the pilot marks an institution’s transition into the operational heart of a new European payment infrastructure. Central to this is the technical integration with the Digital Euro Service Platform (DESP), that provides essential functions like tokenization and alias management that a PSP cannot accomplish alone. Furthermore, PSPs will serve as the gatekeeper for end-user onboarding, while simultaneously mastering smart liquidity management which is based on the (reverse) waterfall mechanism (see “smart liquidity management”).

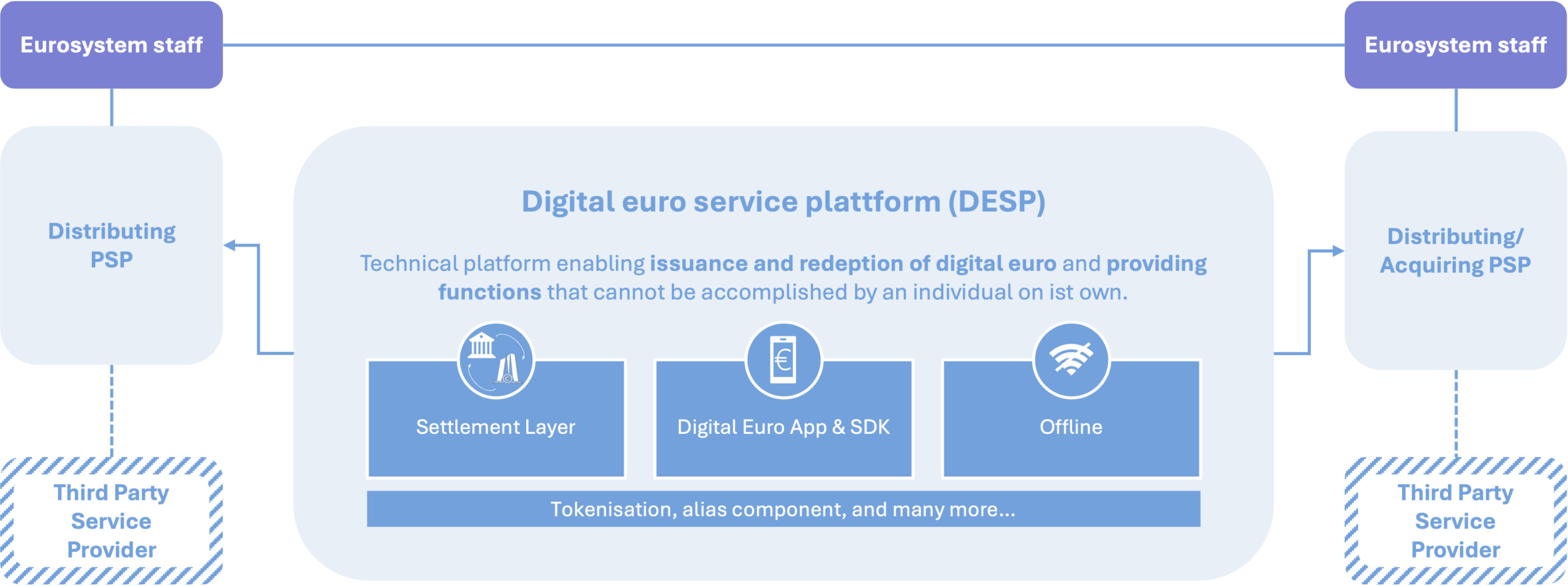

Integration with the Digital Euro Service Platform (DESP)

Integration with the Digital Euro Service Platform (DESP)

A glimpse into the future that the pilot will be shaping can look like this: The digital euro service platform acts as the central infrastructure of the ecosystem, handling core functions such as issuance, redemption, settlement, and key services like alias lookup and secure data exchange. By centralizing these components, the Eurosystem ensures consistent performance and interoperability across all transactions. Payment Service Providers connect via the DESP Access Gateway, using standardized RESTful

APIs and modern industry standards. This alignment with existing industry standards reduces integration complexity and allows institutions to leverage current capabilities. To support implementation, the Eurosystem provides software development kits for online and offline use cases, reference implementations, mock servers, and end-to-end testing tools. These resources help minimize technical risk and reduce development effort for participating institutions.

Smart Liquidity Management

Smart Liquidity Management

During the testing process, the validation of sophisticated liquidity management services, especially the waterfall and reverse waterfall functionalities, has a high priority. These automated mechanisms are designed to ensure that the „beta digital euro“ interacts seamlessly with existing commercial banking money, providing high levels of payment convenience without requiring constant manual intervention by the end user. By establishing a direct link between a user’s DEAN and their traditional commercial bank account, the Eurosystem aims to integrate the new currency into the broader financial ecosystem as a complementary tool rather than a standalone silo.

The reverse waterfall functionality hereby serves as an automated „top-up“ feature for outgoing transactions. If an individual end user initiates a payment that exceeds their currently available digital euro holdings, the system automatically triggers a transfer of the missing amount from their linked non-digital euro payment account to fulfill the payment in real-time, given sufficient combined liquidity. Conversely, the waterfall functionality handles the automated „offloading“ of funds to enforce holding limits. When a user receives an incoming payment that would push their digital euro balance above a specified threshold, the excess amount is immediately redirected to their linked commercial bank money account.

For PSPs, the pilot requires a deep and seamless integration of these mechanisms into their core transaction processing systems. The technical validation to determine if a waterfall or reverse waterfall is required is integrated directly into the pre-settlement phase of an online payment. In specific and exceptional circumstances, such as the processing of concurrent inbound payments where the cumulative total might breach a limit, the pilot also tests an additional post-settlement holding limit check. This ensures that the integrity of the holding limit is maintained even under complex, high-volume scenarios.

Onboarding pilot customers

Onboarding pilot customers

A limited group of around 5,000 end users, that were specially selected from the Eurosystem staff, are directly involved in the pilot to validate technical functionality and provide essential insights into user perspective. This involvement is key to refining the digital euro’s value proposition and ensuring the user experience is optimized before any potential wide-scale rollout. Within this framework, a primary focus lies in ensuring that all technical and operational interfaces enable a seamless onboarding process, with PSPs acting as the primary gatekeepers responsible for managing the entire lifecycle for both individual- and business-customers. The standardized onboarding flow begins with the institution performing necessary identity verification and Know Your Customer (KYC) checks according to applicable regulations. Once a user is authenticated, the PSP requests a unique digital euro account number from the central DESP. The process concludes with the PSP linking the DEAN to the user’s profile, activating their digital payment instruments, and for business users ensuring a mandatory link to a commercial bank account with active waterfall settings.

Strategic Positioning: Perspectives and Considerations of the Banking Industry

Beyond these operational responsibilities, the role of PSPs in the pilot also carries broader strategic implications and as the Eurosystem prepares for the operational launch of the pilot, the European banking landscape around the German Banking Industry Committee (DK) is engaged in a highly differentiated dialogue. While the industry supports the overarching strategic goal of strengthening European monetary sovereignty, the concrete design of the digital euro creates a complex field of tension between state-run infrastructure and private-sector market dynamics.

A central point of debate is economic viability and cost distribution. Estimations for the implementation-costs across the European banking sector vary significantly ranging between €4 billion and €35 billion, suggesting a realistic middle ground between both assessments. Following that, a major point of concern for PSPs is the lack of financial compensation during the pilot phase and the absence of an EU-wide cost-support model for the subsequent rollout. Since core services for end users are mandated to be free of charge, the associations are calling for fair remuneration models to ensure banks retain their entrepreneurial freedom and capacity to invest.

Another argument revolves around possible differences in the regulatory transaction standards of the digital euro compared to commercial banking. To keep things level and ensure a fair competition, many voices demand the same regulatory standards (such as PSD2/PSR). In this context, the industry points to existing, market-ready European innovations such as the Wero real-time payment system. There is a concern that a state-run system could tie up critical development capacities for years, potentially slowing down rather than fostering private European banking initiatives.

Furthermore, discussions do not center on identifying a single defining use case, but rather on clarifying the overall value proposition of the digital euro. Core benefits are primarily seen in features such as offline payment capabilities, access to central bank money, and increased independence from non-European payment providers. At the same time, banking associations point out that, in terms of functionality, the added value compared to existing payment solutions remains limited.

Against this backdrop, their concerns appear partly justified, particularly regarding the risk of duplicating well-established infrastructures. To ensure broad acceptance, the digital euro must integrate seamlessly into daily life without unnecessarily replicating existing systems. In addition, industry stakeholders emphasize the need for maximum security in payment transactions, coherently with the focus of the Eurosystem’s design efforts.

Ultimately, all parties agree on the necessity of holding limits to safeguard financial stability and prevent a massive outflow of deposits from the banking system. The debate focuses on the specific calibration, where proposals range from a restrictive €500 limit advocated by the DK to the €3,000 threshold currently proposed by the ECB.

Following up on those points, the banking industry can view the pilot phase as a decisive opportunity to neutrally validate these points and ensure that the digital euro acts as a non-disruptive complement to the existing monetary order, rather than weakening the proven two-tier banking system.

Why should PSPs participate in the pilot?

Deciding whether to participate in the digital euro pilot is a high-stakes strategic choice. The 12-month phase offers PSPs a unique opportunity to actively shape the future European payment landscape. Within the ECB’s framework, PSPs remain flexible in their frontend integration by either using the reference application or embedding functionalities into their own apps via ECB SDKs, while complying with harmonized UX standards.

The core of the pilot, however, lies in the mandatory „Pilot PSP Feedback Framework.“ Designed as a two-way system, the Eurosystem provides the infrastructure, while PSPs deliver continuous quantitative and qualitative feedback from real-world usage. This data enables the identification of operational friction points and directly feeds into the iterative refinement of the digital euro’s design and rulebook. Participation therefore allows PSPs to ensure compatibility with their business models and technical systems, rather than adapting later to a standard shaped one without their input.

Participation provides a critical technological edge by allowing institutions to achieve technical maturity ahead of the competition. Selected pilot PSPs gain early and exclusive access to the Digital Euro Service Platform and its full suite of specialized development tools, including online and offline Software Development Kits and the ISO 20022-compliant API gateway. By certifying their backend systems and integrating essential user journeys, such as automated KYC onboarding and (reverse) waterfall liquidity management during the pilot phase, banks align their IT roadmaps with the future European standard early on. This proactive approach significantly mitigates the risk of „sunk costs“ and the danger of expensive, last-minute technical pivots that will likely face non-participants when the final digital euro regulation is eventually adopted.

Beyond technical validation, participation in the digital euro pilot is a high-impact branding opportunity that allows an institution to prominently demonstrate innovation leadership to both individual consumers and merchants. Even while adhering to strict communication guidelines, participants are uniquely positioned to test their branding and marketing strategies in a live environment, signaling to the market that they are at the absolute forefront of the most significant development in the European payment landscape.

Ultimately, joining this movement is a decisive step toward fostering European sovereignty and reducing the region’s long-standing reliance on private, non-European payment platforms. By helping to build a single European digital means of payment that is accepted throughout the euro area, PSPs are contributing to a future-proof currency that keeps „our money in our hands“. This strategic alignment with the broader goal of European resilience ensures that the participating banks are not just providing a service but are fundamental partners in a project designed to protect Europe’s financial autonomy and competitive edge in the global digital landscape[6].

Conclusion

The window for Payment Service Providers to decide their position in the future of European payments is closing as the official Call for Expression of Interest by the European Central Bank remains open until May 14, 2026. Participating in this restricted group of selected institutions is the most effective way to ensure that your bank transitions from a rule-taker to an active rule-maker, directly influencing the final design and functional evolution of a future-proof currency.

While the ECB leads this landmark transition, Senacor can serve as a strategic partner to support your institution in the long term with digital euro readiness and the operational mastery of complex features such as (reverse) waterfall liquidity management. Additionally, we use our fundamental expertise to help you fulfil the requirements for the pilot program and support your organization seizing this unique opportunity to shape the next generation of digital payments and secure your institution’s place at the absolute forefront of financial innovation.

Quellen:

[1] https://www.ecb.europa.eu/press/intro/news/html/ecb.mipnews251002.de.html

[2] https://www.ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pdf/ecb.deprep250926_innovationplatform.en.pdf

[3] https://www.ecb.europa.eu/euro/digital_euro/pilot/html/index.en.html

[4] https://www.ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pdf/ecb.dep260305_call_for_expression_of_interest.en.pdf

[5] https://www.ecb.europa.eu/press/intro/events/html/fs_20260320.en.html

[6] https://www.ecb.europa.eu/euro/digital_euro/pilot/html/ecb.faq-digital-euro-pilot.en.html#_Q16_Why_should